September 24, 2014

Advantage, Norway: Top salmon exporters go in different directions

One country's salmon aquaculture embarks on a new round of faster growth while the other sees output taper off.

by Eric J. BROOKS

An eFeedLink Hot Topic

It has been a good year for both Norwegian and Chilean salmon farmers, though the latter had some luck fall their way. Russia's banning of European food products has turned the latter into its salmon supplier of choice. Already rising from 5,000 tonnes in 2012 to 25,000 tonnes in 2013, Chile's salmon exports to Russia can only multiply after its banning of European food imports.

Supply growth drops off sharply

Nevertheless, even though Chile could be exporting near 100,000 tonnes of salmon to Russia in 2015, this represents more of a redirection of trade flows than a rising export market share. In fact, Chile's inability to keep pace with the world salmon market is putting this fish line in a position of possible long-term inflation.

After expanding at a 7% annual pace for the past decade, analyst firm Kontali expects the world farmed salmon supply to increase by a far smaller 3% in 2013 -and for this to be the norm in coming years. The falling growth rate of world salmon supplies is due to the disappointing performance of its emerging market supplier, Chile, though Norway is doing what it can to bridge the supply gap.

Indeed, for most of the past twenty years, Norway has defined salmon farming's technology and business model, but Chile played a vital role in making this once expensive species abundant and cheaper than beef. With its low labour costs, cool Pacific Ocean temperatures, a coastline spanning most of western South America, abundant fishmeal supplies and easy access to low cost Brazilian and Argentinian oilseeds, Chile was for years salmon farming's natural frontier.

Chile's feed supply advantages can be seen in relative cost structures: According to Marine Harvest's 2014 Salmon Farming Industry Handbook, feed comprises 50% of Norwegian salmon farming's total cost but only 43% in Chile. Similarly, in 1990, fishmeal comprised 59% of feed in both Chile and Norway. However, by 2013, Norway's salmon feed was comprised of 48% plant-based meal ingredients and 21% vegetable oils, versus 31% and 18% in Chile's salmon feed.

Rise and fall of Chile

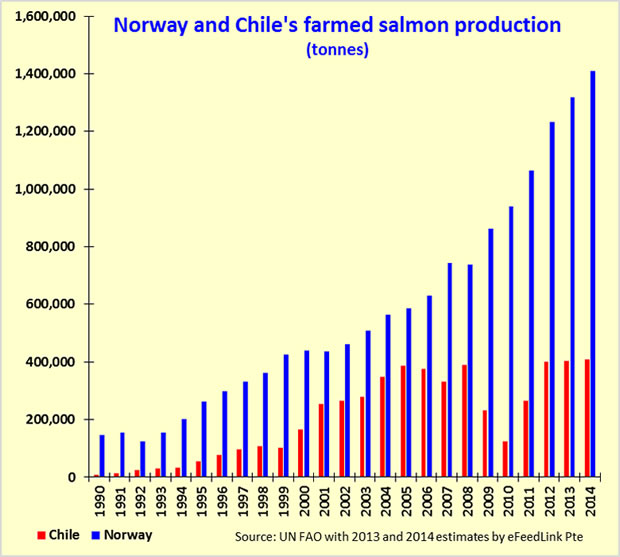

As a leading fishmeal producer, Chile did not hesitate to leverage its relative these feed resource abundance to its advantage. From 1990 to 2000, Norway's farmed salmon output raced ahead 201%, from 146 thousand tonnes to 440 thousand. Chiles's salmon cultivation increased an even faster 1,658%, from a smaller base of 9.5 thousand tonnes to over 166.9 thousand tonnes.

Subsequently, from 2000 to 2005, their two industries kept pace, as both Norwegian and Chilean salmon production increased by slightly over 31% over this time. Thereafter, the tide turned.

With Norway defining salmon cultivation technological frontier, its rapid introduction of new, intensified, yet highly sustainable salmon farming models allowed it to make up for Chile's more abundant feed resources and water acreage. For example, according to Norwegian government figures, in 1985, an average Norwegian salmon cage had a volume of 550m3 , and produced 180 tonnes of salmon annually was manned by 6 workers.

By 2012, Norwegian salmon farms used 60,000m3 cages that produced 1,100 tonnes annually while being manned by only two workers. With each worker producing approximately 18.5 times more salmon in 2012 than in 1985, it was an easy matter to boost output while lowering production costs.

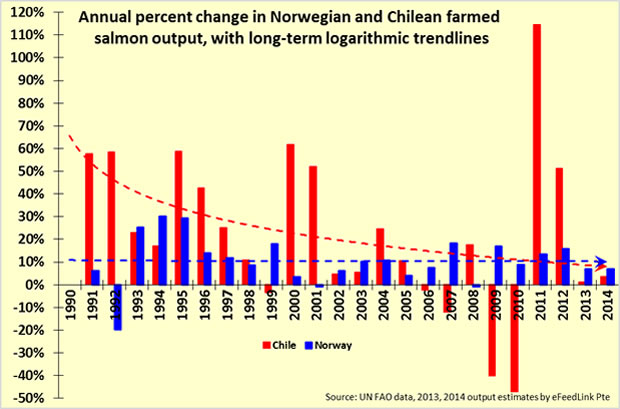

Although the substitution of automated systems and vaccines in place of manual labour and antibiotics was first proposed in the late 1990s, their implementation bore fruit after the mid-2000s. Instead of output growth slowing down as is usually the case in older, more mature industries, from 2005 to 2010, Norwegian salmon output rose 49%, substantially faster than in the previous five years.

Moreover, output growth accelerated strongly from the late 2000s onwards, growing an average annual rate of nearly 13%. Its 5-year output growth rate is much faster than the early 2000s 31% pace; since from 2008 to 2013, Norway's salmon output probably expanded by around 80%.

All this was quite unexpected. In 2011, the UN FAO forecasted Norwegian salmon output to total approximately 1.15 million tonnes by 2013. Instead, 2012 saw Norway grow 1.23 million tonnes of salmon and output of nearly 1.5 million tonnes is expected this year.

Chilean salmon farming, by comparison, has had a most terrible decade. After 2005, efforts at intensification lead to a succession of serious disease outbreaks, such that by 2012, output was less than 3% higher than it had been in the previous peak production years of 2006 and 2008.

Nor has a decade of losses resulted in improved Chilean salmon performance. According to an August Rabobank report, "The deterioration of the sanitary conditions during 2012 and 2013, along with increasing costs and the resulting financial losses for producers, have ultimately been the main reasons for the [latest] slowdown in growth."

Intensification fails, cost higher, output capped

Going forward, a mixture of industry structure and government policies imply that Chile faces more years of essentially flat salmon output and exports. Salmon Rickettsial Syndrome (SRS) is currently continues to infect Chilean salmon ponds, costing the sector an estimated US$100 million in 2013 alone.

Speaking at the North Atlantic Seafood Forum earlier this year, Cermaq CEO Jon Hindar opined that if SRS had afflicted Norway's salmon farms, a cure or way of managing outbreaks would have already have been found. Hindar stated that while Norway's salmon farms contribute to a common R&D fund which quickly creates a science based strategies of controlling such outbreaks, Chile has no equivalent salmon farming institution.

With no salmon farming institutions to manage such crises or share best practises, Chile's government has stepped into the breach, but this too, will have consequences. After seeing attempts at intensification repeatedly devastate Chilean salmon farming for eight years, Subpesca, as the country's under secretariat for fisheries and aquaculture is called, is putting a strict limit on salmon stocking density.

From 2015 onwards, Chile is capping the number of salmon that can be grown within a specific volume of water. Although it hopes this will reduce the incidence of near perennial disease outbreaks, it entails greatly restricting future production increases to nominal, near flat increments.

In fact, even at current production levels, Norwegian executives with operations both in Norway and Chile report that despites the latter's lower wages, Chile's overall production costs remain significantly higher. In an interview with Norwegian publisher mysalmon.no, Marine Harvest CEO Alf Helge Aarskog notes that even at current levels, Chilean salmon production costs remain significantly higher, and much of this is due to the cost of controlling diseases and disease-related losses.

He states that Marine Harvest's Chilean salmon farms, for example, have to be treated for sea lice an unusually frequent once every month. Along with their direct impact on costs, such disease treatments lead to worse feed conversion ratios and correspondingly higher feed intake.

Steady progress in Norway

All this has not been the case with Norway. The country's government has steadily increased the maximum allowed biomass (MAB) for each salmon farm over the years, increasing it by an exceptionally large (but temporary, expiring in April 15 2015) 6% this year. The industry expects the MAB to be increased by 3% to 5% annually, and perhaps more so if a rolling MAB quota proposed by Norwegian politicians is introduced.

Hence, whereas Chile's attempts at intensification met up with disease outbreaks and cost overruns, Norway's capital-intensive farm management techniques and vaccine-based disease prevention has allowed it to steadily increase both the scale and intensity of its salmon farming.

Usually around 10 to 20 metres deep in the late 1980s, many salmon farm cages are now up to 50 metres in depth, with the number of fish stocked per cage also steadily increasing. From 37 million m3 in 2005, total load production volume now is estimated close to 75 million m3.

The Norwegian model leans heavily on vaccines to substitute in place of antibiotics. So much so that less 5% the antibiotics volume used in the 1990s (when output was much lower) is used today. This allowed Norway to grow salmon in intensive, large, densely populated and highly automated cages, without resorting to dangerous antibiotics, as either growth promoters or disease abatement agents. Salmon production costs fell from US$7.00/kg in 1973 to US$4.00/kg in 2006 and US$2.50/kg in 2013. After adjustment for inflation, unit costs fell by more than 90% over the past forty years.

Speaking at the at Marel's salmon "ShowHow" conference in Copenhagen, Denmark on February 5th 2014, Rabobank aquaculture analyst Gorjan Nikolik, states that going forward, depending on how MAB quotas are increased, Norwegian salmon farming output could rise anywhere from 5% to 20% annually, with 5% to 8% the most likely range in any given year.

But with Chile's government effectively capping output after a decade of failed attempts at intensification, Nikolik concurs that there is, "no way Chile will carry on growing after 2015, meaning Norway's will be the driving growth in the industry."

On the negative side for Norway, after enjoying a two decade, spectacular fall in production costs, intensification is starting to exact a toll on the industry. From 2005 to 2013, production costs increased 25% from NOK20/kg to NOK24/kg. While this is not a bad performance in light of rising costs for both fishmeal and plant-based feed ingredients, it does belie that intensification still carries a trade-off relative to salmon performance.

This year's warmer ocean temperature and intensified production have caused a recurrence of a sea lice problem, with infestation levels equal to their peaks in 2010 and three production regions reporting very high infestation levels. In fact, some executives are urging the government to go slow in expanding the MAB, openly stating that they fear too large of an increase could lead to a repeat of Chile's disastrous disease outbreaks.

According to Salmar CEO Leif Inge Nordhammer, over the past 10 years, sea lice and pancreas disease losses and treatments have boosted production costs by NOK8/kg to NOK15/kg. This however, only comes out to 1.2 to 2.5 cents/kg more since 2005. It has been dwarfed by the past decade's rise in feed costs and productivity increases of the past ten years. Indeed, with feed costs falling by far more than salmon prices, margins should continue to improve.

Going forward, the only question is if Norway can extend its ten year run of boosting salmon production via continuous intensification without running into disease outbreak bottlenecks. Kontali estimates that its output grew at a 6% annual rate from 1997 to 2012, with the rate of increase accelerating above 10% after 2007.

Rabobank is optimistic, with Nikolik stating that, "In two or three years' time, possibly due to technological innovation, the salmon farming industry is likely to solve many of the biological and environmental issues that are currently being tackled." That in turn would allow Norway's government to increase salmon MABs, allowing for greater intensification and for rapid output growth to be maintained.

On one hand, this means that even if the intensification of Norwegian salmon cultivation creates short-term problems with sea lice or other maladies, this country will have moved past any short-term production interruptions by the second half of this decade.

On the other hand, one must distinguish between innovation and implementation, with Chile not having been particularly successful at the latter. Despite the warmer (and less healthy) ocean currents off Chile's coast, many Norwegian integrators are heavily invested in Chile and have a stake in boosting its salmon rearing productivity. In fact, despite the current pause in Chilean output growth, it has more potential to boost salmon output over the long run than any other country in the world.

From 6.5% of Norwegian salmon output, Chile farmed salmon production totaled 65% of Norway's before falling back to approximately 30% this year. Until either Chilean salmon farming recovers its growth momentum (by mastering intensification), the current spell of high salmon prices could go on for at two years and possibly longer.

Consultancy Fishpool stated that in wake of the market turbulence caused by Russia's ban, early September 2014's average salmon price of NOK33/kg (US$5.20/kg) and Q4 futures contract at NOK39.90/kg, "is as low as it gets." It expects the price to rise by NOK2/kg (US$6.28/kg) every month into the first half of 2015, by which time salmon could cost NOK50/kg US$7.09/kg). That would put salmon beyond its record peaks of NOK44-45/kg seen in 2006 and 2011. -Except that feed costs are lower than they were in 2011 and non-feed expenses are lower than they were in 2006.

In fact, at the North Atlantic Seafood Forum, many Norwegian executives felt confident that they could leverage better disease management and falling feed costs to cut production expenses from the current average of NOK24/kg to near NOK20/kg within two years. In fact, even without lower feed costs, Kontali estimates that getting both pancreas disease and sea lice fully under control would result in savings of NOK2/kg to NOK3/kg.

Consequently, with prices poised to stay strong for up to two years, plant-based feed costs falling and fishmeal prices poised to either stay flat or decline, this is a good time to be a Norwegian salmon grower.

All rights reserved. No part of the report may be reproduced without permission from eFeedLink.