FEED Business Worldwide - January, 2011

The changing face of global poultry

by Eric J. BROOKS

Due to its unique combination of efficient feed conversion ratios, capital-intensity and ease of transport, no livestock line has grown more strongly than poultry. Going forward however, the next decade will see a slowdown in broiler output growth, with domestic, in-country production expanding faster than exports.

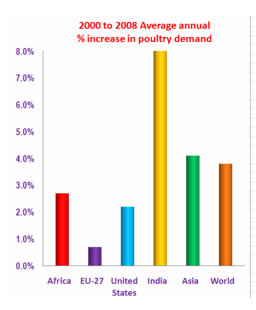

This will be quite a change, as poultry exports rose at cumulative annual rate of 6.2% per annum since 2006. That year, they totaled 6.55 million tonnes but in 2011, the USDA expects poultry exports to amount to 8.95 million tonnes. Yet, according to a recent report by the joint University of Iowa – University of Missouri 's Food and Agriculture Research Institute (FAPRI), the 2000 to 2008 3.8% per annum gain in poultry output will be roughly halved over the next decade.

Production, exports decelerate

Assuming the recovery continues in developing countries, FAPRI projects that world poultry output expansion will decelerate to 1.8% per annum. By 2019, poultry production will have increased by 17.4% over 2010. This year's 67.60 million tonnes will have risen to 79.36 million tonnes by the end of this decade.

Over this same time period, poultry exports will rise at a meager rate of 1.3% per annum, or 12.3% in total, from today's 7.38 million tonnes to 8.29 million tonnes by 2019. With production growing marginally faster than actual poultry trade, exports will fall from today's 10.9% of world output to 10.4% by 2019.

The tapering off of export growth reflects a shift in the type of countries that are growing quickly. Both quantitatively and percentage-wise, India and Russia will experience the greatest increases in broiler production but as massive, self-contained markets, they are neither export-oriented nor import-dependent. Russia in particular is using domestic poultry production as a means of import substitution. China, which was once an exporter and is turning into an important importer, is watching its maturing consumer demand for poultry grow more slowly. These coinciding factors are dampening overall export growth.

Even so, within regions themselves, we see considerable variation. For example in Asia, India's near double-digit poultry production increases must be set against near static supply and demand in Singapore, Japan and Korea and slowing market growth in China.

Integrated Russia, unconsolidated India lead expansion

Within the EU-27 nations, poultry production will rise less than 1% per annum, the lowest increase in the world. Except for Britain and Germany, western Europe is raising fewer birds than before. Yet, within Eastern Europe, led by non-EU member Russia, the years 2000 to 2008 saw poultry production skyrocket by 21% per annum, from 1.2 million to 3.2 tonnes.

Within the EU-27 nations, poultry production will rise less than 1% per annum, the lowest increase in the world. Except for Britain and Germany, western Europe is raising fewer birds than before. Yet, within Eastern Europe, led by non-EU member Russia, the years 2000 to 2008 saw poultry production skyrocket by 21% per annum, from 1.2 million to 3.2 tonnes.This amounted to a whopping production increase of 175% over eight years - with 105% of that massive 175% increase occurring in just one country –Russia. Similar large increases in broiler output are underway in neighbouring Hungary and the Czech republic. Yet, it is solely because of Russia's ongoing poultry expansion that Europe, while losing its exporter status, still accounts for 15% to 16% of world broiler production.

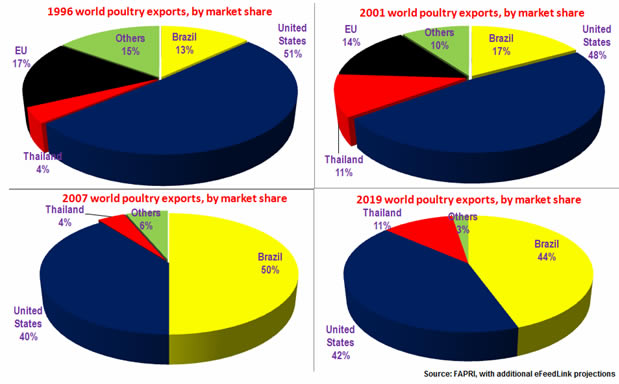

Russia's rise however, is making life more difficult for export-oriented poultry producers. With up to approximately 30% of US broiler exports usually heading for Russia, that country's rising poultry self-sufficiency and import protectionism did much to place America into second place behind Brazil, which now leads the export parade.

Faced with Russia's import substitution strategy, Thailand's CP opted to forgo mass exports to Russia and is establishing integrated feed to chicken processing facilities in that country instead. Indeed, CP's strategy in Russia is a carbon copy of its China strategy, where it set up numerous feed to broiler facilities over the past two decades.

CP's presence in Russia also demonstrates another important difference between the two vast and self-contained Indian and Russian markets. Whereas India's poultry sector remains made up of numerous backyard suppliers, 86% of Russian poultry is raised by large, very modern integrators - The difference being that Russian integrators, unlike their Thai, Brazilian or American rivals, remain focused on the domestic market and are not export-oriented at this time.

Despite Russia's stellar output growth, Europe's role in world poultry market is in secular decline. By 2019, the continent will be a net importer of 29,000 tonnes of chicken annually. An EU AGP ban, high feed costs, costly animal welfare rules and environmental laws undermined European producers' competitiveness. Going forward, the EU's greatest influence on global poultry will be its import safety standards, as European rules for supplements and AGPs are strict.

America holding its own, Thais to retake Brazilian gains

Trade-wise, more changes will occur in poultry's import demand than in its supply base. Perhaps the decade's most important shift has been the EU's transformation from exporter to importer status and America's large (though controlled) market share loss. Both gave way to ascending Brazilian poultry exports.

Trade-wise, more changes will occur in poultry's import demand than in its supply base. Perhaps the decade's most important shift has been the EU's transformation from exporter to importer status and America's large (though controlled) market share loss. Both gave way to ascending Brazilian poultry exports. Indeed, thanks to Thailand's post 2004 bird flu troubles, it will not exceed its 2003 poultry exports until approximately 2011. In that respect, Brazil filled in gaps caused by falling Thai production amid rising world export demand. Such successes aside, our survey finds that Brazilian poultry's terms of trade are becoming tougher. Consequently, the next decade will see Thai broilers regain EU and Japanese customers which substituted Brazilian poultry in bird flu's wake. US broiler exports will increase by approximately 3% annually while Brazilian exports flatten out, allowing the former to claw back some of the latter's market share.

On the other hand, powered by rising ASEAN growth rates and AFTA's liberalisation, Thai poultry exports will rise 6.5% annually over the next decade. The Thai export share, which almost sank below 4% in H5N1's aftermath, and which is currently 6.6%, will rise to 13% or more by 2020. FAPRI projects net exports to rise from this year's 370,000 tonnes to 2019's 645,000 tonnes. This will mostly occur at Brazil's expense, which will decline from 50% of broiler exports to a still dominant 44%. Even so, our survey concluded that for Thailand, regaining market share entails considerable investment, feed sourcing and political risks, which our country survey explains in greater detail.

While the American share is approximately 39.6% at this time, given the topping out of Brazilian export markets, NAFTA liberalization and falling dollar, US exports will growing faster than world poultry production. By 2019, America will account for 41.7% of poultry exports, putting it only a shade behind Brazil.

China, ASEAN the new import markets

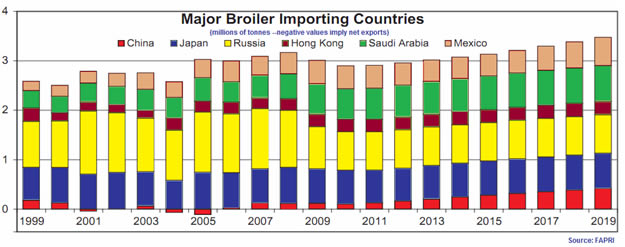

With regards to imports, the greatest inflow will be into north Asia and to a lesser extent, Southeast Asia. Amid growing consumer demand, feed shortages and high input costs, China's World Trade Organization (WTO) liberalisation is transforming this former broiler exporter into a net importer. While its trade was roughly balanced over the last decade, FAPRI sees imports firmly outpacing exports over the next ten years. By 2019 the country is projected to import 418 thousand tonnes of poultry meat, far more than the EU.

With regards to imports, the greatest inflow will be into north Asia and to a lesser extent, Southeast Asia. Amid growing consumer demand, feed shortages and high input costs, China's World Trade Organization (WTO) liberalisation is transforming this former broiler exporter into a net importer. While its trade was roughly balanced over the last decade, FAPRI sees imports firmly outpacing exports over the next ten years. By 2019 the country is projected to import 418 thousand tonnes of poultry meat, far more than the EU. Just offshore China's coast, FAPRI expects neighbouring Taiwan's per capita chicken consumption to rise 20.9% over 10 years, from 24.9kg today to 30.1kg in 2019. To meet this demand surge, Taiwan chicken meat imports are expected to grow by 7.3% annually, from today's 61.5 thousand tonnes to 116 thousand tonnes in 2019. Indeed, the only parts of the Taiwanese poultry sector expected to survive are specialized, price-insensitive lines and which involve the rearing of traditional Chinese broilers.

In Asia itself, imports by South Korea, Indonesia and the Philippines are also expected to grow in response to overall economic expansion and liberalization in these markets. With AFTA and CAFTA at their backs, Thai integrators should lead a charge of both exports and capital investment into ASEAN, north Asia and China. Indeed, our Philippine survey discovered that Thai capital investment inflows will be an act of mercy to a Philippine broiler sector incapable of reforming itself.

Russia - the country to watch out for -

Yet, if there is one importer we should watch carefully, it is Russia. –Its 1.7% annual growth in chicken consumption is being outraced by 4.7% annual growth in output. According to RosBusinessConsulting, poultry imports accounted for 28% of Russian chicken consumption in 2009 but only 22% in the first half of 2010. It states that Russian poultry imports fell by 19.4% in 2009 and by almost 20% in 2010.

For several more years, this will merely result in Russia driving out imports and recapturing its domestic market. However, in the second half of this decade, the country may transition to being a significant –and technically state-of-the-art poultry exporter. For it must be noted that 62% of Russian poultry rearing enterprises have been built since 2006, with many new investments in new, integrated facilities. This wave of capital investment is coming both from government subsidised local integrators and multinationals such as Thailand-based CP.

Determined to be self-sufficient in meat, government policies in BRIC poultry importers Russia and India will induce in a stepped up pace of integrated poultry investment. Consequently, the next ten years could see domestic broiler output catch up to domestic demand. At that time, we could see Russia's emergence as a poultry export powerhouse.

In such a situation, given the geopolitics of food and feed, it is very likely that China will opt to import broiler meat from Russia rather than America. This would coincide with a gradual consolidation of India's poultry sector, which may seek subcontinent markets in Pakistan, Bangladesh, Nepal and Bhutan as its primary export outlets.

BRIC countries localising poultry production

Taken together, we are seeing a restructuring of the poultry industry and its trade flows. In a nutshell: BRIC country policies in India and Russia are making global poultry go local: While exports are still growing, they are doing so more slowly and trade is becoming more regionalized.

In the future, Thailand will ship more of its exports to ASEAN and less to the EU. Indian subcontinent countries are more likely to rely on Indian exports. China, if it can, would prefer to import broiler meat from neighbouring Russia rather than America.

Brazil, which came out of nowhere in the 1990s to become the leading exporter, will see its share cut back to pre-bird flu days, just a tad ahead of the United States. Thailand will leverage new ASEAN export capability, overseas investments and a recovery of its EU and Japanese exports to regain the world poultry market share it had achieved in the early 2000s.

Up to now, smaller countries such as Brazil and Thailand have served as export platforms. In the future, with large, inwardly directed markets such as Russia, India coming to the fore, trade will become more regionally oriented in nature. This is especially true of Thailand, where AFTA trade liberalization has seen its poultry exports surge into Southeast Asian countries such as Vietnam, Philippines and Indonesia.

Nevertheless, with trade growing more slowly and large countries focusing on self-sufficiency, future discussions of world poultry will concentrate more on foreign direct investment into such countries and less on chicken parts being transported across national boundaries - And below, we survey poultry industry prospects within the national boundaries of its most important production, consumption and export centres.

The above are excerpts, full versions are only available in FEED Business Worldwide. For subscriptions enquiries, e-mail membership@efeedlink.com